|

Session

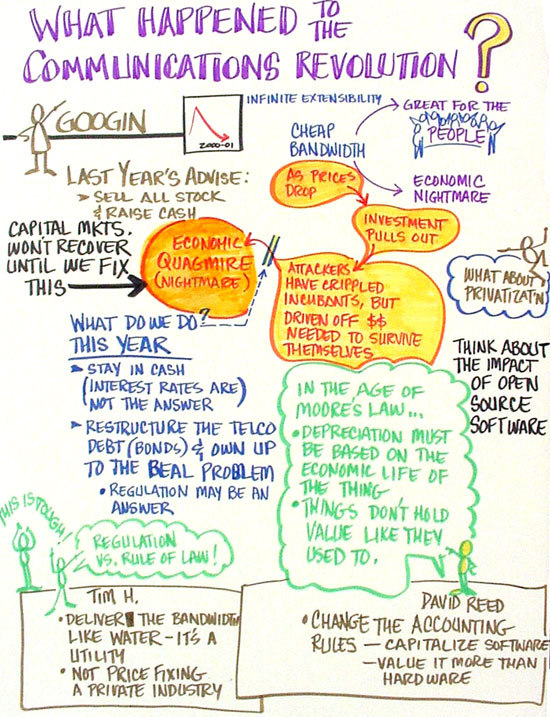

2: Holy halibut! What happened to the Communications Revolution?

Wednesday evening,

September 5, 2001

David Isenberg:

Roxane, you have five reward-minutes for being right last year.

Roxane Googin:

Last year I was very politically incorrect in my fairishness. I learned

a lot from this meeting last year. I run a strategy advisory service

for portfolio managers. I've listened with great interest because people

were talking about the core of the Internet. I spoke earlier about the

hourglass [model] and how the best network is one that is totally generic

so that you can't tell one bit from the next. That is the beauty of how

this network works. You can project on to it what you need to do. Also

the network is infinitely extensible, [because] we have DWDM. I walked

out of this conference [in 2000] and told all of my clients to sell every

stock that they owned as fast as they could.

Isenberg: How

come you didn't tell me?

[laughter]

Googin: And

raise cash. The reason for that is . . . a system that behaves like that

is an economic horror show. It is going to repel capital because any

system that is totally generic has no barrier to competitive entry. You

can't differentiate yourself. One that is infinitively extensible means

that you are going to be stuck in a Malthusian swamp, where your cost

of selling will be one inch above the marginal cost of production.

Both of those scenarios

are going to repel capital. I knew that, so the goodness of it on one

hand was a nightmare economically on the other. It is a paradox. And

just like oil, society is going to benefit the most if bandwidth is the

cheapest because then we can project all of this stuff on to it. But

if bandwidth is the cheapest, no one is going to be there to build the

bandwidth. So what I saw happening is that the cat had been let out of

the bag, the genie was out of the bottle, and people were building these

networks and we were headed for this huge train wreck whereby capital

would start pulling away from this industry once they realized that this

was going to happen.

So

the attackers with the new technology were going to starve to death because

they weren't suppose to be cash-flow positive yet, cause they've gotta

build this huge network. As prices come down your network has to be bigger

before you are profitable so it was working against them. So

the attackers with the new technology were going to starve to death because

they weren't suppose to be cash-flow positive yet, cause they've gotta

build this huge network. As prices come down your network has to be bigger

before you are profitable so it was working against them.

And then on the other

side, the incumbents (and I'm going to be a little general here and you

can disagree with me but this is how I see it) are slowing going bankrupt

on their own, some quicker than others, and I'm talking not only the BTs

and the DTs and the FTs and the NTTs and the ATTs and the Worldcoms and

the Global Crossings but the RBOCs too because their SONET-based networks

have a cost of provisioning up here [high].

But even though the

attackers are starving, they are forcing the marginal bandwidth prices

below the RBOCs' cost of provisioning -- not only replacement but provisioning.

So the RBOCs are going to get squeezed because they have this complex

labor intensive infrastructure that is no longer supported by the economic

base. So you have this kind of nightmare scenario where nobody wins and

it is just a big mess because the attackers are going under but they have

crippled the incumbents.

What we are witnessing

is the perfectly predictable outcome which is no equipment sales, and

no more progress. No one planned this, but it is too late to turn back.

The other problem

is the phone companies don't own their gear -- it is leveraged. That is,

they bought it forward in time. These guys have 20/30 years bonds outstanding

against their SONET gear, because this was never suppose to happen.

We are looking at

the worlds largest single businesses, I think. (I don't know if they

oil business or car businesses is bigger, but it is one of the three.)

The business has been rendered economically dead because of a real important

piece of progress that has come out that acted differently than anyone

planned.

Those 30 year bonds

that were funded on the continued operation of this SONET gear will never

be paid back. Those insurance companies, those orphans owning those bonds,

the asset that they were buying against will not be economically viable

in 20 years much less two.

So not only is their

capital base being rendered useless, but now they are supposed to reinvest

in a bunch of new gear. They are obviously not doing it because they

can't.

This is what I envisioned

when I walked out of here last year. I got kind of freaked out. But

it is manifesting. If you listen to what is going on in Europe, DT just

fell below its offering price in 1996 for the first time. NT&T continues

to slide, France Telecom, British Telecom, they're at multi year lows.

And it continues to get worse.

We live in interesting

times. I don't want to call it a problem but it is certainly is something

that is . . .

[laughter]

Man: Do you

have any bad news?

Isenberg: What

happens next?

Googin:

Well and that is really interesting cause I would like everyone to join

in on that one. One thing that I do for my clients is I predict trends.

I never predict the future, OK? There is a difference. And I'm just trying

to think if I had a big idea that slipped out here. Googin:

Well and that is really interesting cause I would like everyone to join

in on that one. One thing that I do for my clients is I predict trends.

I never predict the future, OK? There is a difference. And I'm just trying

to think if I had a big idea that slipped out here.

Man: You mean

parts of the twelve you have already given us?

Googin: So

what do we need to do, we need to restructure the entire industry but

how.

Man: We socialize

the risk.

Googin: I agree

because . . .[somebody boos] . . . but I've got to finish.

Man: That is

a sure way to loose.

Googin: Yeah,

well they did pretty good with the interstate system and . . .

Man: They subsidized

all of the truckers at the expense of the railroads. Why was that good?

Roxane: That

was a good point.

Man: Why in

the world would you subsidize the risk? I don't want the damn risk.

I didn't buy the bonds.

Man: . . .

in your IRA . . .

Man: No I don't.

Man: Yes you

do.

Isenberg: Roxane,

finish.

Googin: The

last paradox is that we want it dirt-cheap. We can talk about what we

are going to do. It sounds like you have some good ideas so I want to

hear.

We want it dirt cheap

because then it can be as good as it can be for all the other economic

things that it is suppose to do. But it can't be so cheap that it repels

capital. OK people keep asking me well what do I do with my stocks? My

answer is stay in cash, until . . . but when will things get better?

They will get better when we fix the problem, OK?

Everyone is watching

Greenspan cut rates. If interest rates have been 22% and he took them

down to 3, then you could say interest rates caused this. But interest

rates have nothing to do with this. This is technology problem, so interest

rates aren't going to fix it or impact it one way or another.

You can go to Japan

and see 11 years of decline with 0-percent interest rates. So we have

to fix the problem. This means restructuring the debt and owning up to

what the real issues are. This owning-up hasn't been done yet.

Then we have to reallocate

the assets to the right parties. Unfortunately some markets don't behave

in a traditional market way. This is something to think about. Typically

common good markets, like transportation systems, tend to be regulated

markets, because the capital outlay upfront is associated with an unknown

return in the future. This regulation is rather contentious, whether it

is the old telecom, the airlines, or even trucking. There are just some

markets that don't behave well, and I'm afraid that this is one of them.

So we have a lot to think about.

Man: I would

infer that you're saying there has to be a re-regulatory impulse.

Googin: We

should debate that here. That is out of my area of expertise.

Man: I'm just

asking you whether or not the inference that I'm drawing is correct that

there has to be a re-regulatory impulse because the private market is

not going to get there fast enough.

Googin: I don't

know if the market will ever get there. I think . . . regulation -- my

limited imagination could come up with that.

David Reed:

I have a suggestion for 2 reasons. One is, I wrote an article four years

ago called, "Accounting in the Age of Moore's Law," which said,

until we fix this we are building something that is equivalent of the

savings and loan crisis.

I came out with a

different answer about what is going to turn it around. The point was

that in the age of Moore's law, if you just think in terms of depreciation,

that is the right way to think about it, what is the depreciation life

time of something where technology is doubling every 3 years, 1 year,

or whatever it is, in capability? The depreciation should be based not

on how long the equipment lasts but on how long the equipment is competitive.

Googin: The

economic life.

Reed: The economic

life. It is clear that we now have history in the communications industry

that the economic life is very short. So you cannot issue a bond that

is any longer than 3 years. And that doesn't make economic sense.

Man: Not true.

Man: Well hold

on. You have to recognize that you are arbitraging long and short, if

you are going to do that.

Man: Or you

are betting that you can change the rules, what 'legal' means?

Reed: Two things

have happened. One, for a long time the telecom industry has lived in

a regulatory environment that has forced it to use long depreciation lifetimes

and assume that it is will get pay back on equipment. It can't live in

that environment anymore; there are too many ways to solve the same problem.

Googin: And

thank heaven equipment is cheaper.

Reed: And second,

we expense software, except software's economic life time is much longer.

So my argument was that, for a long time, this was OK because software

and hardware bundled and it sort of came out right. We were depreciating

the wrong thing and not depreciating the right thing but they were in

the same place. So nothing really mattered.

Then we unbundled

the two. We had protocols and applications, and we had connectivity.

That destroyed the world. The only way out is to stop assuming the value

is in the hardware and start capitalizing the software, the infrastructure,

the applications, the way that they should be as a lifetime asset.

Tim Denton:

When you speak of regulation you engage a zone . . .

Reed: I was

not saying regulation; by the way, I was proposing accounting rule changes

that are consensual agreements analysts have with companies, right?

Denton: I would

like to speak of regulation and the difference between regulation and

the rule of law. This is a general discussion point about these things.

When you play hockey

there is competition between the players within a bounded rink on a certain

ice with blue lines that are drawn. And the net is a certain size. That

is the rule of law. There's also regulation, which is enforced by the

referees, to determine whether high sticking or elbowing is going on.

One of the things

that makes markets work, and what an obsession with markets fails to understand,

is that they work in a context of a rule of law, whereby you simply just

can't take out the head of the grocer because you disagree with his pricing

decisions. So we all live in a zone which is determined by a rule of

law.

When you speak of

re-regulation, you may very frequently be thinking about something, which

is actually a rule of law issue rather than a regulation issue. When

I think of a regulation, I think of a bureaucrat or functionary of the

state setting a price, determining output, or something like that.

Now here we have a

situation where the problem is that there ain't no money in it so but

it is manifestly good that [e.g.] we get clean water. So we have taken

clean water and we have put it in to the domain of something that is delivered.

We have taken a function, we have made it so simple and so cheap that

everybody gets it. So perhaps what may happen is that when we get bandwidth,

which is, there is just no money in bandwidth and yet it is so manifestedly

good for everybody to have tons of it, that we may socialize the risk.

We may just turn it

into water delivery. So in a true Internet fashion the transport is just

taken care of, like the interstate highway system, [while] the applications

continue to be totally competitive.

So I've changed my

topic in a sense, but what I wanted to say is before we talk about regulation,

let us just be clear that we are not talking necessarily about someone's

setting a price, we are talking about somebody creating a legal framework

in which investment can take place in a rational and orderly way. And

my panic meter goes into the red when I hear re-regulation if we assume

that what we are really doing is taking a private sector of monopolies

and setting prices and outputs in the old fashioned way.

Man: We did

a great job re-regulating Amtrack in the United States˜

Man: California

did a great job of reregulating electric power.

Man: So maybe

some issues are settled by a framework of a rule of law as which competition

proceeds rather than that a bureaucrat determines prices and output.

Reed: There

is border crossing. Somebody explained to me that Louis Brandeis, when

he was serving on the Supreme Court, wrote a decision about regulation

that basically said, in considering economic questions you are not allowed

to consider economic extranalities. That was the way it was explained

to me. So network externalities, like scaling laws or whatever, could

explicitly not be considered in the context of either set of rules.

Denton: David,

I didn't understand a word that you said. Your point would be?

Reed: My point

would be that driving these fine distinctions about what's regulation

and what is not is not really so simple. Because judges are perfectly

happy to rule on meta-points as well as what kinds of rules are allowed

to be made.

Denton: I'm

just saying that society might set up laws that might permit the solution

of this problem that would not involve constant price adjustment by bureaucrats,

lawyers . . .

Man: In time

the industry will work its way through to earn return on invested capital.

It is just a matter of time. Michael Porter's five forces generally determined

profitability of an industry. It is not so much what a regulator is going

to do about the industry -- how many competitors do you have in an industry?

And over time this industry will consolidate its way down eventually it

has to because it will not get any more increases in capital until it

starves itself

Man: Which

is the other option. There are only 2 options, either you reregulate the

industry or you completely deregulate the industry. We are kind of in

the mid-way point, no one really knows, we kind of want to deregulate,

but we don't really.

Man: Tim when

you say "reregulate" would you please unpack what you mean by

that term.

Isenberg: In

which dimensions?

Man: [I think

he means] socialize and build out fibers to everybody's homes. Everybody

shares the fiber plant.

Man: Private

companies can do it. Public companies can do it. The point is that there

is a framework of law in which a bulk commodity is delivered very cheaply

for a lot people.

Victor

Blake: First of all, communications is [governed by] interstate law.

I'll remind you that a very small fraction of the global population of

the world actually gets municipal water, including me. I get private

water. Victor

Blake: First of all, communications is [governed by] interstate law.

I'll remind you that a very small fraction of the global population of

the world actually gets municipal water, including me. I get private

water.

Isenberg: And

you are going for a civil engineering degree . . .

Blake: Civil

engineering degree, right. Communications law, particularly in the United

States, would make a very interesting. comparative study with other countries.

A lot of the problems that we have are probably related to that. There

are functions that appear to be legislative law -- by the people, for

the people. But most of the law is actually administrative law with a

very poor history of case law. If you understand how case law works,

particularly with administrative law, the best analogy for telecommunications

regulation in the United States is actually immigration law. It is horrible

because of the way that you establish a single incident by a decision

of a judge. This does not involve public oversight or public decision

making. It is essentially private decision making. That is in fact how

telecommunications law has been proceeding over the United States over

the last 70 years.

Adina Levin:

I just wanted to say if Roxane had any more suggestions I wanted to hear

them.

Googin: I would

like to hear what every one else thinks. I think it is urgent. Our network

economy is not going to manifest until we figure this out.

Isenberg: That

is why we are here.

Googin: Time

is of the essence. The reason that sales are down, blah, blah, blah,

is because this is just draining the vitality of the entire economy.

On the margin this is where our growth [has been] coming from, and it

has stopped. It would be helpful if someone in Washington knew the problem,

and could actually say it rationally. Then I think the more ideas the

better. I can identify the problem, but I don't think I'm qualified to

solve it.

Peter Ekelund:

I want to say I wholeheartedly agree with your conclusions. I think all

of us here might be academically right. [But] we have created a completely

impossible business to invest in. Unless we are figuring out a way that

makes economic sense, unless we want to re-introduce socialism, we better

figure out a way to make economic sense of investing in this business.

I think that that

should be our strong focus, not how to create these wonderful ideas.

But a very, very stringent laser focus on how to make money on what we

have created. Otherwise people will all die. I'm very optimistic about

doing that but frankly, to listen to people around here, it has not sunk

in yet how serious it is.

Jonathan Thatcher:

Yeah, I certainly underscore all of the above. When I hear about legalities

and regulation law and communism and all these other things being thrown

in˜.

Man: No one

has said communism.

Thatcher: I

would like to go back and use water as an example. In my own mind that

makes a really lousy metaphor for one simple reason, and that is the delivery

of water over the last 2000 years has not technologically improved dramatically

at all. Decisions on what is good for society [regarding] something that

does not move and is not inherently chaotic in its advancement, is a simple

process that has significantly low risk.

But [we are discussing]

something that we don't really know and understand, and we don't know

where it is going to go, or what we can we predict in 20 to 30 years.

To say that any group of people can get together and can noodle out the

right way to create the environment that is the optimal solution for the

technology -- this just doesn't make sense to me.

The only thing I know

of in the history of the world that has been successful at making any

sense out of chaos, unfortunately, is capitalism. And capitalism given

enough time will in one way or another refine the chaos into something

that may not be ideal but at least has order and has benefit.

Man: I want

to go back the idea of repelling capital because of the price of provisioning

is so close to the price of resale. It seems to me that there are businesses

that have high capital investment cost but are nevertheless sold on very

narrow margins, like the cooper business. Take any commodity market.

Googin: DRAMs.

Man: DRAMs,

red winter wheat, light sweet crude oil -- the kind of market where when

the price goes up competitors come in, and when the price goes down, competitors

exit without causing these cataclysms we are seeing. Can we get from here

to there or are there aspects of this market that keeps this from being

a commodity market, a spot market for bandwidth?

Googin: We

could do that, but I think that the infinite extensibility that we apparently

have with DWDM . . . it takes you a little while to dig up the coal and

you do have different people's cost of recovery . . . I have a whole other

theory but this isn't the right time about the post-Newtonian economy

. . .

Man: You keep

saying that there is something unique about bandwidth, that theoretic

demand for is infinite.

Googin: No.

Man: How is

that any different than the business of making Pentium processors? The

supply of computer processing power is infinite, and increases at roughly

the same pace, and it is incredibly capitally intensive, yet Intel has

made more net profits than any other company in the world since 1971.

Man: They had

70% market share.

Man: Yeah,

but they don't have any government involvement or any socialization .

. .

Man: We won't

have 11 networks in the United States from 5 years from now, one way or

another, we will be down to 3.

Man: I would

like to point out that your characterization for the bandwidth market

is not at all unique. There is no difference between that commodity and

any other commodity.

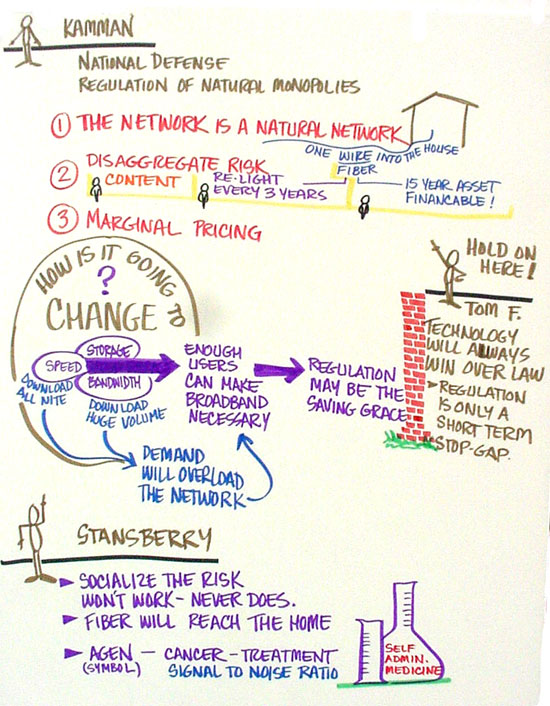

Steve Kamman:

Adam Smith, the father of capitalism, said the government exists for 2

reasons -- national defense and the regulation of natural monopolies.

If you are going to look me in the eye and tell me that this is the fixed

line network, not the wireless network which is another natural monopoly

cause there is only so much spectrum.

Isenberg: Steve's

5 minutes have now started.

Kamman: I'm

an ex-telecom guy who switched to being an equipment guy. I was at MCI

and I am older than I look. I start with sort of 3 base line points.

First, it is a natural monopoly.

Man: What is?

Kamman: The

network. At the absolute last mile, when you get down to it, it makes

more sense to have 1 wire to have 2 wires. Now we can talk about wireless.

We can also talk about how we get access. We can also say from a societal

point of view, I would prefer a society to invest in one wire. Now the

nice thing about it is that if I just have that one wire it is a 30 year

asset. Maybe it is only a 15 year asset, maybe it is only a 10 year asset,

but it is an asset I can finance with debt with some certainty. Talk

to the Worldwide Packets guys.

Man: Only if

you block other initiatives.

Kamman: Before

you say no, keep the mind open for a little longer . . . The fiber is

a 15-year asset. What you light it with, how you light it, what you send

down that pipe, who owns it, is not a 15 year asset. What you have here

is a fundamental shift where in the good old days the network and the

application were tied to each other. It was a network and it carried voice.

Today the physical asset is still something that you did a trench for

and you shove it in the ground and it sits there.

Man: You have

been reading me.

Kamman: If

I put a fiber in there, I can stick whatever I want on it. I can finance

that fiber with, say, 15 year debt, say, 10 year debt. I can go out and

legitimately say I can deliver X dollars a month by selling a fiber to

somebody else. They take on 2 additional risks: [First,] technology risk.

What am I going to light it with? That is going to change every 3 years.

I've got to take on a risk -- I need to relight the network every 3 years

in order to stay competitive. Then the other risk, which everybody wants

to bundle in to that same network, is the content. Well, I don't want

to take the content risk if I am taking on the lighting risk. Somebody

else has to figure out what is going down that pipe.

So we disaggregate

the industry. And somebody owns the boring 10 year asset that they finance

with boring old debt. Somebody else owns the middle part -- maybe that

is just the plain customer. If I'm going to light my fiber into my home

with something really old and slow because I don't want to upgrade, that

is my problem. Nobody comes in and tells me that I have to upgrade my

bloody refrigerator. Whenever I want to buy a new frig . . .

Then, the last item,

somebody else takes the risk of what am I going to put in the frig. Well

that is my problem. Number 3 is marginal pricing. The reason marginal

pricing is so bad is that the traditional network cycle (and this is where

it is different from cooper) when I first build a network, it has a potential

capacity of, say, 100. But I only sell 10% of it. And then over time

I sell more. The marginal cost of the next bit is almost zero, so that

is how I make my money. Somewhere in the middle I cross over and suddenly

every additional bit is pure gravy. The big problem is right at the end,

when the marginal cost per bit goes through the roof because the fundamental

architecture of my network wasn't designed for that many bits. So I'm

throwing a lot of capital to get that next marginal bit out.

Man: ADSL

Kamman: That

is ADSL, that is SONET. OC-48 was suppose to be a core backbone product,

and we are selling it on the edge. The problem is that if I build an

asset with a 10 year life and, I price it on a 10 year life, and it turns

out to be a 5 year asset. I'm screwed! So the problem is that you are

dealing with these screaming marginal costs curves. We as a society would

argue that there is a societal interest.

You have to walk up

to that guy who is saying, "I don't want to sell you more bits because

it costs me too much money, I loose money on every bit that I sell."

And you've got to kick them off the cliff.

So the debt holders

finance the network, and then the equity holders get the returns at the

end. [The solution is that] right at the end you have to kick the equity

holders back off and put it right back to the debt guys who get the next

10 years worth of spending.

When I am e.g., driving

my fully depreciated taxi cab, the last thing that I want to do is to

buy a new cab. In New York, every 5 years you have to buy a new cab.

I don't really care whether the old cab is working or not working. Every

5 years, new cab, finished. You can do that or you can go to Washington

D.C. and the cabs never˜.

How is this going

to change? And I'm just convinced of this: we are so bandwidth centric

in this world. Remember there is bandwidth, there is processing, and

there is storage and they are effectively substitutes for each other.

If I have all the bandwidth in the world, I don't need processing, and

I don't need storage. All the storage in the world and da, da, da . .

. If I had all the processing in the world, I could compress the Internet

into one 8 kilobit thing. Send [???] like zen.

Remember this, because

right now what we have is a bandwidth bottleneck. That is not going away,

because there is no way to finance it. Now you'll have some stuff on

the edge, and have some stuff on the margins. But people will take advantage

of the fact that processing and storage are still hammering forward according

to Moore's law. Particularly the storage out there is going to get so

bloody cheap that I'm going to replace storage for bandwidth.

How do I do that?

I will just tell them it is a critical mass of residential broadband.

If you get enough users out there . . .

Man: What is

the cheapest way to do it?

Kamman: Storage

right now, without a doubt. The point is, I am going to need a lot of

megabits to do streaming, or I need a lot of hours to pull that thing

down, dump it in the thing and then pull it out of local cache. To an

end user it is the same problem, same result, same solution. I'll take

the cheapest solution -- water finds the lowest level [e.g.] big Tivo

boxes. Even better, a friend of mine just downloaded his whole CD collection

on to a hard disk simply because it allowed him to play random play.

The day that I get broadband and the day that he has broadband is the

day that I ask him to email it to me.

[laughter]

Man: This is

your answer to Napster.

Kamman: Absolutely

but here is where it goes back to the network. So you start see to see

groundswells. If you get enough people using ADSL, they'll use it in

ways that they never thought. That's how they do Napster. You come in

at 11 o'clock at night, you tic, tic, tic, I want all these songs and

then it downloads all night long. That is how people do Napster. Eighteed

hours a day, while you are asleep or at work, that your little DSL modem

is going to be sucking stuff out of the network.

The network is not

built for everybody's DSL modem turning on when everybody is away at work

trying to suck down vast quantities of content. It blows up the networks.

How do we know that? It is exactly what Napster did to the campus LAN.

It is going to happen all over again. What happens then?

Then the consumer

comes into the equation. Why can I shut off all the Northpoint? Because

it is a bunch of geeks. Hey Northpoint, click you are gone, you guys

don't vote, I don't care. I know, it is 150,000 geeks but the senate

doesn't care. When AOL went to flat-rate pricing the whole network browned

out. Suddenly AOL had 2 choices, number 1 tell its users to go pound

sand -- over time, we will get to it -- typical Telco response. Number

2, you nearly go bankrupt throwing capital at the network and then run

away from it as fast as possible and outsource it to everybody else.

Why did they choose option 2? Because, remember it was on the cover of

Time magazine. The FTC was about to fine it. It had senate holding hearings.

Cause you had enough people who were started to depend on the Internet

. . .

I'm not saying this

is good for the telecom industry. I'm saying that broadband is going

to get dragged kicking and screaming out of the national economy one way

or another because if you get enough people out there that want it, then

the demand is going to increase, then it is going to become irrational,

then the best hope is regulation. It is the only way we will get a decent

return on that asset.

Isenberg: Hang

on here. We have two more panelists. Thank you.

[applause]

Tom Freeburg:

I used to work with a guy who pointed out that every problem, no matter

how complex, there is a solution that's appealing, simple, easy to understand,

which is not exactly the same way as simple, elegant, and wrong.

That suggests that

too many of us are falling into the simple thing.

By the way, there

is a stock market in bandwidth, as a lot of us here probably know and

a few of us that have even played in. We keep thinking about bandwidth

as a natural monopoly just like the railroad barrens thought about transportation

as a natural monopoly. Hey guess what guys? Technology has outstripped

that. It is too blooming late. You can't make that stick much longer.

I have a 2-hour speech I like to give on economic models and how that

it affects telecommunications.

Man: Please

give it now!

Freeburg: It

is when the world changes the people that owned the world before, go nuts

and they try everything that they can to change it, FUD, uncertainty and

doubt, legislation, all sorts of things like that. We are in the FUD

arena of telecommunications moving from a natural monopoly into something

where entirely different laws apply. By laws I mean natural laws, not

written-down laws. And as we all know, as the whole Napster thing clearly

illustrates, the world is changing and the legal system can't possibly

keep up with it.

History tells us you

can't pit law against technology and expect law to win. At best law can

sweep the tide back for a very short period. That is all that is gone

on right now. It can't possibly come out any other way. Technology is

going to win. There are just too many ways to deliver bandwidth. And

people are using bandwidth in too many new ways. By the way they are

going to use it in ways that we haven't even thought of yet. It is all

over, it really is.

I spent a lot of effort

explaining to my bosses that broadband cable was going to win over DSL

because broadband cable allows a number of different companies, different

entities, to use the same cable to transport [???] without having it look

exactly the same and without having to thread through even the same business

organization. It allows entrepreneurship but DSL doesn't.

Isenberg: Let

me point out that the very definition of natural monopoly has technology

in it. So if the technology changes then than the natural monopoly changes.

Larry quick comment?

Larry Lessig:

Just a quick disagreement with this. In the long run it doesn't matter,

but nobody wins in the long run. In the long run we are all dead. You

could have said the technology of radio would not have admitted of this

-- commercial control of radio was produced by the FCC when the FCC was

captured by radio in the 1930's and 40's and 50's. You could have said

that technology would not allow that and eventually radio will be liberated.

Well maybe if Dewane gets his way in 20 years, that will happen. But

still we had a 100 years of the technology being distorted by the legal

process being captured by special interests that had an interest in stopping

the progress of technology. So this is a happy story about how technology

wins in the end. But where we are right now is in a world where strong

interests are trying to stop the progress of technology in a way which

is hampering [???].

Isenberg: Now,

let's get back into the panel. Porter Stansberry is a free marketeer

to beat all free marketeers -- take it away!

Porter Stansberry:

I'm going to try to be very succinct. I write a newsletter and you can

all find my newsletters. I publish 4 different newsletters, one of which

I write . . .

Isenberg: No

commercials!

Stansberry:

pirateinvestor.com,

Isenberg: No

commercials!

Stansberry:

I've got 5 minutes to say whatever I want.

Isenberg: Free

marketeer, bullshit!

[laughter]

Stansberry:

Anyway the password that you will need is Big Hook.

Isenberg: Hey,

no commercials!

Stansberry:

Well, the user id is BigHook and the password is 2001, so go priinvestor.com

and enter Big Hook, 2001. And in one minute I am going to summarize what

happens to all the networks in the world. The bottom line is that it

was very, very bad business. Between 1998 and 1999 capital expenditures

for telecom companies doubled, but revenues didn't come close to doubling.

That was a sure sign of that we were in the midst . . . [Tape turns over]

. . . The other thing

that people should have noticed was in 1994 AT&T's revenues peaked.

So you have the leader of the industry suffering declining revenues 6

years into it, it is a sign that piling on is not necessarily the best

idea. The real problem is the narrow pipes to the user, because what

you are building was not supply but capacity, and there is a difference.

So there is an over-capacity problem. There is no such thing in economics

as a problem of over supply. Supply drives demand, price change. So

in the future what is going to happen is optics will come into the local

loop, and finally supply will come on line. Over capacity will solved.

All that won't happen if you socialize the risks. They socialized the

risks of Japan's banking system in 1990 and it didn't get us anywhere.

If you go back all through history, socializing the risk in any industry

freezes it in time, and nothing ever changes. Going back to the railroad

analogy, the first private railroad in the United States was James Hills

Northern Railroad. It was wildly profitable and it didn't receive any

government subsidies in an arrow when, supposedly, the costs of running

a railroad were below the price of [???]. So these problems have all happened

before and the answers were never social. The answers were always entrepreneurial.

Man: Rent control

in New York City.

Stansberry:

Another great example. And there is no such thing as a natural monopoly,

that is just total crap. If there would be, government would regulate

real estate, they don't, so forget about it.

Isenberg: Except

for rent control in New York City . . .

Stansberry:

Right -- it doesn't work. I have something more interesting to talk about

with my remaining 2 ½ minutes. It is much more valuable re: the signal

to noise problem, and that is the treatment of cancer. I have been spending

a lot more time on that this year because there is no money to be made

in telecom. Anyway, briefly, there is a great company that you guys should

all take a look called Antigenics, out of New York. The symbol is AGEN

and it trades for $16.50. The market cap is 500 million dollars. They

have an extremely successful, well proven vaccine, a therapeutic vaccine

for cancer. The technology is called heatshock protein and the signal-to-noise

problem is that in cancer your body has a tumor that grows that is made

out of your own cells, so it does not trigger your immune system. Your

immune system does not detect cancer is being a foreign invader so it

does not react. Antigenics takes a sample of your cancer tumor, you specifically,

extracts something called the heatshock protein, which is a signal of

your immune system and then delivers that signal directly to your immune

system over a 2-day process using Federal Express.

Man: Oh, that

is hot.

Stansberry:

This is first commercialized program of individualized medicine. When

people say we wasted all this money on the Human Genome Project, it is

an example of people not understanding the difference between a technology

and a killer application. I made a point earlier about the combustion

engine beating the technology carving the application. In this case,

genomics is the technology, but the application will be individualized

medicine. It is going to happen in a lot of forms. The first one will

be treatments for cancer because cancer is unique to the individual.

So a phase 3 trial

is going right now for kidney cancer, should be finished in 2003, approval

in 2004. It will be a $20,000 treatment and it replaces chemotherapy

and radiation. As soon as it is approved for one cancer, it can be used

off label for any cancer. The technology is not cancer specific but patient

specific.

The second trial they

have going on right now is in pancreatic cancer. They get 40% success

rates. Kidney and pancreatic cancer are both 99% fatal, pancreatic cancer

within 12 months. So the testing process can be very quick, the burn

rate right now for the company is between 6 and 10 million dollars a year.

They have 80 million dollars in cash. Garo Armen, CEO, took Imunex public

and had a 12 year career at Goldman Sachs. When he discovered the technology

in 1994, he resigned his job, became CEO. The first doctor that they employed

to run the first clinical trail left his practice and became Chief Medical

Officer. I have about 10% of my net worth in this stock.

Woman: And

what was this company name again?

Stansberry:

Antigenics, AGEN.

Man: What entrepreneur

funded all the basic research that went to that genetic information?

[laughter, applause]

Stansberry:

The government spent 3.5 million dollars on the human genome project over

a 10-year period and another company named Celera, in 6 months beat all

that with less than a 300 million dollar investment. And now nobody is

using the public database because it is no good.

Isenberg: You

know, there is summer tradition in Woods Hole called the Friday Night

Lecture at MBL. They invite the people who are gonna win the Nobel Prize

in the decade to come and talk. Or in rare instances they are late and

they have Nobel Prize winners. Craig Venter spoke 2 weeks ago and he

was awesome. I went because of [Porter Stansberry]. What do you say

about the average employee at Celera? There are 24 year old math Ph.D's

from the top of their class who ride skateboards down the hall and . .

.

Stansberry:

I was doing a comparion between Amazon.com's average employee and Celera's

-- at the time they were roughly valued the same.

Isenberg: Anyway,

so somebody whispered in my ear this is the first time I've seen a corporate

logo at one of these Friday night lectures -- because, in general, they

are all academics. Venter was awesome. Thank you very much for that.

Stansberry:

Sure. I bought my stock for $11 in January.

Man: Why are

you telling us this?

Stansberry:

I'm telling you because I thought it was a much more profitable example

of the signal-to-noise problem.

Man: If he's

right, he gets twice as much time next year.

Isenberg: Now,

that is the real commodity.

Stansberry:

And I think that the problems of the network are pretty well understood

and I think that they will be solved, hopefully in market ways over the

next 5 years.

Victor Blake:

Can I ask a question? One thing that nobody has really discussed yet is

privatization of networks. We've talked about network operators and service

providers with the vision that that is how networks should be built.

It you were to take a look at transportation as an example, one can conclude

that cars are simply the privatization of transportation -- as opposed

to railroads.

One point of information:

you probably don't know that AOL runs a huge number of private networks

that are not on public carrier networks that carry approximately 75% of

AOL's gross traffic volume between data centers. They are on 3 year depreciation

schedules for capital equipment and 10 years for the fiber. It is very

agressive --these are privately owned and privately capitalized by AOL.

Kamman[?]:

Regarding transportation there is another way to look at it if you think

about marginal costs. For example, in L.A. they stopped building new

freeways because the next freeway doesn't really change traffic patterns.

The problem is that the individual still wants to own his car, but looking

at the collective cost, in 200 years we will have to do something. I

don't know what that is. But at some point you have to scrap the system

and either build different cars, or force everyone to buy motorcycles,

or force everybody into trains, or do something different, because otherwise

L.A. starves.

Blake: In D.C.

we call it the toll road. It is a private enterprise investment and it

is actually profitable, as I understand it.

David

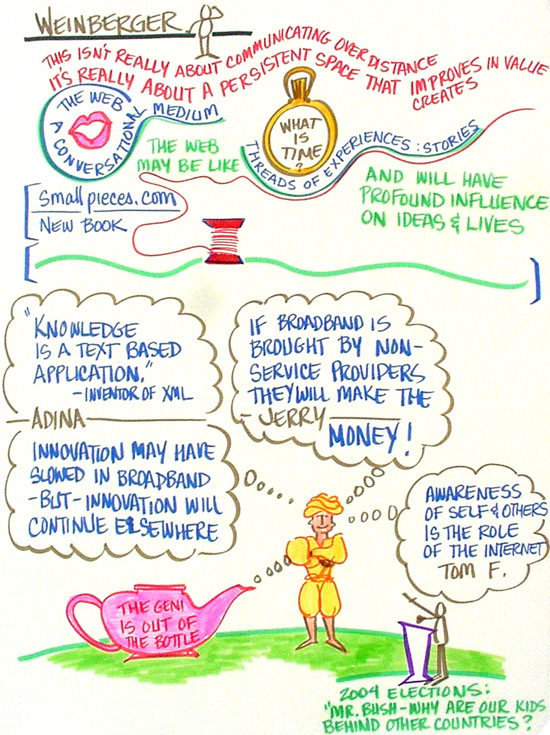

Weinberger: I don't really understand any of this. But since I am

standing I will continue. Did you just see a blinding light of fear washing

over me? I was going to talk about the telecommunications revolution

and why it hasn't done what we have expected it to do. David

Weinberger: I don't really understand any of this. But since I am

standing I will continue. Did you just see a blinding light of fear washing

over me? I was going to talk about the telecommunications revolution

and why it hasn't done what we have expected it to do.

The first thing is

that I don't look at this as a telecommunications revolution at all because

it is just not my area of interest. What I care about is not so much

the questions of provisioning bandwidth, which I understand is a crucial

question. I don't look at this as telecommunications at all. Telecommunications

is communicating over a distance and I don't think that the Internet or

the Web is really about communicating over distances.

What's remarkable

about it is that it is a persistent space. It is a space that accretes

value over time. Every page that is put up and every discussion that

gets added to adds to the value of the web. That is really different

than what the telecommunications infrastructure was built for -- telephone

calls -- it has nothing to do with that.

So I think of the

Internet as a persistent space that accretes value over time. I, like

Jerry, just turned in a book draft a week ago, so I'm in this nervous

state of waiting to hear what my editor says about whether it is done

or not. So I would like to talk about this by talking about a book that

I was co-author a couple of years ago, and then tell you what the theme

of the new book is. Is that a plug? Oh well, too late!

Man: David,

just tell us what you have to say. Stop apologizing.

Weinberger:

I will apologize as long as I want. Back off! [laughter].

Well the first point

was persistent space accretes value. The second point is that what The

Cluetrain Manifesto said to me is still basically right. It came out

during the height of the positive hysteria about dot.coms. The reason

why the Internet jangled our cultural nerves is not that it is a big opportunity

for some 25 year olds to make a lot of money (but that's nice too). What

we think is exciting about it is that it is a conversation medium that

enables people to have conversations in the literal sense, and then in

the extended sense.

Conversation, in this

case, is people who are talking voluntarily, because they are interested

in the same thing. They are speaking in their own voice with some passion,

about something they care about. That is the characteristic of the web

that has made it such an object of interest and passion. It is not really

that we move some business functions online, although that too is important.

But if that is all it was who would give a shit about the web? Something

else was going on, and Cluetrain suggested that conversation is a metaphor

[???].

The book I just maybe

finished is called, Small Pieces Loosely Joined. I wrote it on the web.

I posted drafts. You can read it, in its unfinished entirety at smallpieces.com.

I haven't talked about this in public before.

What it tries to say

is that what's important about the Web, the biggest effect that the Web

will have will be on ideas, in fact, better ideas of our culture, things

as basic as space and time and matter over reality and knowledge and public

and groups and self and morality. In fact, those are all chapters in

the book.

As I was writing I

realized the chapters are getting repetitive so I decided that that must

be a theme. The theme seems to be . . . let me give you an example of

how I think this works. So we have a theory of time that says -- I'm not

saying that this is a well worked out theory -- but if you ask most people

what time is, if you really push them on it, like in a Philosophy 101

class, they tell you about moments of time and the march of a string across

the knife edge of the now, little tiny quantum, moments of time.

We know that the more

you think of that the less sense it makes; the more paradoxes, the more

contradictions. The most important thing is that it has nothing to do

with how we experience time in our own lives in the real world. We don't

live a series of moments. Our lived experience of time is not of discreet

moments, it is of events. It is 5 minute stretches of our turn to talk.

Or our College years. We have a complex of stories that we view time

in -- threads if you want.

That

is not in accord with our every day philosophy about time, which is of

discreet moments, so we live with some alienation. Now you go to the

Web or the Internet, there are explicitly called threads. The Internet

has this threaded nature. It feels like a set of complex rivers that are

going by, like Heraclitus' Rivers, which were always changing, but there

is a river there, you can step into it. That

is not in accord with our every day philosophy about time, which is of

discreet moments, so we live with some alienation. Now you go to the

Web or the Internet, there are explicitly called threads. The Internet

has this threaded nature. It feels like a set of complex rivers that are

going by, like Heraclitus' Rivers, which were always changing, but there

is a river there, you can step into it.

So there are email

threads, there are discussion threads. My 16 year old daughter has 6

IM sessions opened at the same time. Each of those is threaded within

itself and there maybe some weaving of threads. Even on Ebay, when you

are bidding on an auction that is a story, that is a thread -- you can

go back to it, it has an end that you can reread later on, if you are

really bored.

So web time turns

out to be a lot like our normal everyday experience of time, which is

very different from our abstract explanation of time. That may be one

reason why our experience of the web feels both alien and new, but also

very familiar and very comfortable. [It explains] why hundreds of millions

of people can step into this radical new technology that is disruptive

and it doesn't feel disruptive at all. They feel completely at home.

It is because the experience of time and space and other things on the

web is, in fact, so much like our everyday experience and so unlike what

we have been telling ourselves that experience is about.

So if it is true that

the big effect of the web is on ideas, that the web should be viewed not

just as a technology, not just as an infrastructure, not just as an economic

vehicle but as an idea, the way that democracy is an idea, it arose as

an idea, it had its effect as an idea. If the most important thing about

the web is in terms of an idea, of course the revolution hasn't happened

yet. It takes a long time for ideas to work their way into our lives

and to have practical affects on our lives.

[applause]

David Reed:

David, I would like to offer you an alternative title, which is that there

is many stories in the naked Internet.

[laughter]

Isenberg: Well,

do you want to keep going for another half hour?

Jerry Michalski:

David, it sounds really wonderful. Thank you. That was a great first

talk. It was really excellent.

I want to tie what

you said back to where Roxane's started ask an open question. There is

implicit assumption about capitalism that I've been making for a long

time that I'm beginning to question: that there is no business without

barriers to entry. [Roxane] said that nobody will invest in a business

that doesn't have barriers to entry, because it gets competed down to

nothing, and who wants to make nothing on nothing.

Basically, capital

will flee a market where there is no clear lock, where you don't have

a lock on a patent or a barrier to somebody getting into your business,

where commodity isn't profitable. Maybe it is worse than that -- that

the commodity will never get built if something is instantaneously commoditized.

Also let me tie it

to what Tom was saying earlier -- if Motorola suddenly started building

Metricom-style devices that everybody could buy and install in their home,

that wirelessly connected to one another and created a high speed Internet,

no carrier would own the Internet. No carrier would have the last mile.

We would just provide it for one another and it would heal itself if the

software were good enough. It would be essentially free. Whether bandwidth

or storage or processing was the cheapest, it wouldn't matter, because

those things would chase each other over time. Motorola would make a

bunch of dough from that, just no carrier.

Anders Fernstedt,

who I met through David, made me realize that what 3G means to carriers

is a return to the advanced intelligent network. They plan on corralling

location information about me and selling that to advertisers. They plan

on having control over a lot of info about me that I have no desire for

them to have. And it is not just 3G, it is a whole bunch of old business

models about scarcity and barriers are [still operative].

I've

been hunting on the web and everywhere else, for post-scarcity economics.

What happens when there is abundance? What happens when things are inexpensive

and available and there are few barriers. And what happens when companies

build loyalty because they've done good work and they are just closer

to you and they get what you do better. You don't want to leave them.

It is not because they made it really hard to export your data from Yahoo

groups, or some other strange reason. They are perfectly happy for you

to go someplace else but they are doing stuff better for you than anything

else is. I've

been hunting on the web and everywhere else, for post-scarcity economics.

What happens when there is abundance? What happens when things are inexpensive

and available and there are few barriers. And what happens when companies

build loyalty because they've done good work and they are just closer

to you and they get what you do better. You don't want to leave them.

It is not because they made it really hard to export your data from Yahoo

groups, or some other strange reason. They are perfectly happy for you

to go someplace else but they are doing stuff better for you than anything

else is.

Forget branding.

I'm not talking about branding at all, because branding is indirect, expensive

marketing.

Levin: A lot

of the discussion in this room has been about how do we pay for bandwidth

when telecom companies are trying to depreciate 30-year equipment. Right

now, capital markets have stop funding bandwidth. This is a big problem

because this has stopped innovation. If we're in the bandwidth business,

it is a tragedy.

But if we are talking

about the changes caused by the industry, email is already a killer application.

Tim Gray, one of the guys who invented XML has a great quote on his website

saying that knowledge is a text based application. So we are talking

about the killer applications and people that are providing bandwidth

wanted it to be true that radio is the killer application. But a lot

of what is interesting doesn't necessarily require high bandwidth. If

you have a network and it connects large numbers of people who can talk

to each other, that is already a heck of a lot. I think that this is

going to be an unpopular opinion in this crowd, but I think that there

is an amazing amount of innovation you can do on narrowband. That is

point one.

Point two is that

when we talk about having a space that is based around conversation, that

is based around archiving conversation and sharing thought based on editing

conversation, it was done once before, it is called the Talmud. And the

rabbis whose accounted what we now know of Judaism had conversations over

long periods of time and took them down and edited them into these fundamentals

documents. This record is very different from the linear organized way

of thinking that we get from the Greeks. I think we are going back to

a paradigm that people did without technology that now could be easier.

Isenberg: Good.

Freeburg: Just

a few real simple points. I will submit that the killer application for

the Internet is awareness. What people really want is expanding their

sphere of personal awareness, expanding it geographically, expanding it

in terms of social content, expanding it in terms of knowledge. All such

applications are increasing in their demands for bandwidth. The telegraph

took a lot less bandwidth than the telephone, and the things that we are

using today take a lot more.

Second is that all

attempts by governments or quasi-governmental organizations to control

the spread of new technology have in the end failed.

I like your argument

that in the end it may not matter because we are living in the now, except

that remember, the Internet didn't exist as a public phenomenon 10 years

ago. I'm sorry. We have to live out the eventuality. It is happening

too fast in comparison to previously technological changes for it to make

any difference. The automobile, by the way once it took off, absolutely

changed the life inside of a single generation. This is going to be that

much faster.

I have a couple more

pretty simple points. We are having a discussion that leads me to think

about the differences in the way that the French and the Germans approach

the evolution of language. For those of you who don't know it, the French

have a state committee for the preservation of the French language that

is very careful. Whenever a foreign word they don't like gets into the

language they invent a French phrase using existing French words to substitute,

and make it the legally required [language]. The Germans, on the other

hand, have a committee for the extension of the German language that adopts

new words very happily.

We have to be careful

about the difference between teaching the old paradigm and being sure

that for heaven sakes we don't break out of the box, and being aware that

we have unleashed the genie, he is really out of the bottle all together,

but the genie we've unleashed doesn't come in terms of bandwidth or in

terms of fiber, it comes in terms of humans communicating with humans.

By the way, not in real time necessarily.

Remember this sphere

of awareness includes not only other people, it also includes events in

near real time and a tremendous amount of human knowledge, and unfortunately,

a lot that pretends to be knowledge and really isn't. One of the speeches

that I have given in the past in my role as Chief Futurist, I talk about

how we are going to have to develop critical thinking, which is something

that they used to teach in school, so that we are very careful to not

allow our real belief system to be mislead by something just because we

read it on the Internet or in a newspaper. By the way, this exact phenomenon

happen back when the publication of newspaper was first invented. All

of the same stuff that we are talking about happened then.

Eric Best:

I will give you my coupon. To this point about old economy, old economics,

scarcity and barriers, were the models based on abundance? Just briefly,

in 1981-2 I was writing editorials in California and I got really obsessed

with the idea that the centrally-planned economies were doomed in the

face of information technology. What would become of them? They would

just collapse around an internal contradiction.

A couple of years

[later], stimulated by Reagonomics, I thought there must be a internal

contradiction in capitalism if we could only figure out what it was.

Then I had a fellowship year and I spent time going through the Harvard

Library trying to find anything between socialism and capitalism. So

I was looking for something called communal capitalism, but it wasn't

in the card catalogues in the Kennedy School or the Harvard Library, or

the Business School.

Actually you really

didn't hear about it until Clinton started using the phrase, which was

kind of interesting -- what was he talking about? I've been on this journey

for a while in the company of Napier [Collyns]. We were in a meeting

in London at one point in '92, '93,'94, talking about the restructuring

of Europe and what was going to be happening with the technology. I found

myself thinking, 'Oh I'm still in this same kind of quest to understand

is there a contradiction in the capitalist model.'. Now I think, 'Yes

there is', and I think I know what it is.

It's how do you protect

proprietary models in an open information architecture in the knowledge

economy, where you are moving from scarcity of physical objects to the

infinitude of ideas. If you have a knowledge economy where ideas are

essentially unlimited, and they are stimulated by the fact that everybody

has access . . . In fact if you believe that the economy is driven by

supply, is in your interest that more and more people get connected in

order to have more and more ideas, so that those ideas and those derivatives

will produce economic stuff. Therefore, it is in the public interest

that access ubiquity matters. Connectivity matters. So do you think

that connectivity and awareness will be extended fast enough to enough

people to produce this abundance if there is no intervention in the free

market? I think, and I would like to be seen as somebody speaking personally

not as a Morgan Stanley representative . . .

Best: We know

that the free market doesn't do a really good job allocating education

to everyone who needs it, or healthcare to everybody who needs it. So

if everybody needs connectivity the way they decided that everybody needs

a toilet, I suggest we should consider that some intervention might be

needed, if you think the knowledge economy requires connectivity and that

the free market is not actually providing it fast enough because the margins

aren't there, or for whatever reason.

Kamman: As

much as I was passionate before, I am going to get cynical again here.

I remember what Adina said, we were taught a lot more about whether or

not we needed some government action last year. And I would say the mood

in the room when you mention government was much more negative then it

is this year.

What has been interesting

for me to watch, now that I'm an equipment analyst, is that Motorola can

make a lot of money by selling that device, which by the way Robert Berger

is actually building. The equipment guy can make a lot of money by selling

that device. The guy who sells the services on it may not. If you want

to talk cynically, my guys, the equipment stocks, probably won't come

back until broadband comes back. When broadband is something that the

telecoms resist, those guys start to say, "Hmmm our customers and

us are headed down different paths."

Man: Where

is the broadband coming from if the demand isn't there> And how does

the demand get there if the last mile isn't there?

Kamman: Talk

to B2. The point is that you have to make the last mile happen. At some

point in time B2 will . . . the Koreans have 60% DSL penetration. It

does come, but what is the social force that will come in and speak for

it. Intel's stock doesn't come back up until broadband kicks off. So

how does Intel make more money? They start lobbying, because Intel worked

it out. Microsoft is going to work out that the only way they make money

is in broadband.

Man: By the

way, Intel said that gigabit Ethernet is their highest priority.

Kamman: That

is another way to look at it. You get another force in society that starts

going out there and starts throwing money at a party.

Man: How does

that play to your assertion that bandwidth and processing power are interchangeable?

Kamman: I think

what happens is the consumer is going to find a way to suck down stuff.

When enough consumers start sucking down enough stuff, I think it just

breaks the network, period. The beauty of a broken network is that consumers

get angry. The lesson of AOL's problems a couple of years ago is that

15 to 20 million angry consumers get listened to. 10 million angry consumers,

7 million angry consumers don't get listened to. But if I get another

angry consumers out there, then I tip the balance. Then we will solve

this problem.

Ekelund: Can

I give you an argument why I think the U.S. will start deploying fiber

very quickly? It is probably the only argument that actually will beat

the shit out of all of you. You are the biggest country and the most

powerful country that controls the world. Let's assume now I said to you

that Stockholm has 100,000 users using 10 to 100 megabits all the time

sending videos to everyone all the time. And we decide to say here is

Atlanta, Bell South, a shit network. Let's try it out, let's send 10,000

Pearl Harbor movies to them and see what happens. Do you know what is

going to happen? It is dead. If you were the Security Advisor of the United

States . . . are you going to be an isolated world power?

I think this is the

simplest arguement for you to start -- that you are not a world power

if you don't have the biggest broadband network in the world.

Man:

I am the Democrat running against George Bush 4 years from now and it

is the debate. Man:

I am the Democrat running against George Bush 4 years from now and it

is the debate.

Isenberg: I

hope so!

Man [putting on

southern accent]: Mr. Bush, why is it that an American child doesn't

have the same access to DSL as a Korean, as a German, as Swede? Why is

our nation behind? Is it because of you?

[laughter, applause]

Man: Why are

you from the South?

[laughter]

Jonathan Thatcher:

I just want to let everybody know that I think that there is a glimmer

of silver lining in this cloud. This is going to sound really bizarre,

especially to the investors in the world. As I look out at the last couple

of years that we have spent working with customers what I have seen is

hundreds of potential customers. They are not all real customers. There

are hundreds of potential customers with hundreds of different business

plans. They run the entire gamut of pure capitalism to pure communism

including Red China. I've seen every combination and permutation that

I can imagine of ways to bolt together a business proposition to go forward

and be successful for a community, for a business, for a -- you pick the

entity.

Somewhere in that

morass there are going to be a couple of successful models. I don't know

which ones that they are. As we architect our systems and we go sell,

we don't try to pick which they are. We try to pick the ones that seem

the most reasonable. But there will be a number of them. And we can

speculate what they are going to be, and we probably should. It would

be helpful if we had an idea. But I'm confident, I'm incredibly bullish

on the idea that the inherent competitive environment that we have created

on a worldwide basis [???] the midst of this chaos to find out that winning

set of propositions that are going to be successful. Maybe it just takes

patience. I believe that if we wait three to five years, we are going

to see those things bubbling to the top.

Man: Can you

just answer a question, maybe with a pie chart. What percentage of the

business plans you have seen are financed by long term junk bonds? What

percentage is financed by equipment-vendor financing? And what percentage

is financed by equity?

Isenberg: A

generic answer will suffice; a pie chart is not necessary.

Man: I think

that it is different from country to country.

Thatcher: I

would say that on a global basis, the ones that are going to step forward

and put the money on the line are communities and municipalities who are

tired of waiting for broadband connectivity.

Man: It is

really government bonds?

Thatcher: It is happening

outside of Tier 1 cities, it is happening on the other side of the digital

divide and that is the momentum is coming from in this country.

Man: Technically,

municipalities are corporations. [???] telecom municipal bonds.

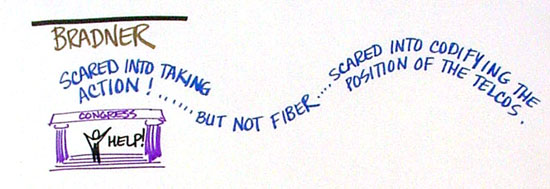

Scott

Bradner: I would like to tie together a couple of the last conversations.

We were told that we needed to be scared into doing the right thing, and

that would be the only way that it would work. Well it happens that we

are being scared right now˜ Scott

Bradner: I would like to tie together a couple of the last conversations.

We were told that we needed to be scared into doing the right thing, and

that would be the only way that it would work. Well it happens that we

are being scared right now˜

Isenberg: I'm

scared!

Bradner: In

Congress this week the regional telephone companies are scaring Congress.

They are scaring Congress by saying that broadband will not be deployed

(and their definition of broadband, of course, is a straw not a fire hose).

It will not be deployed unless they are ridded of the onerous task of

opening up their networks. Congress is not unlikely to pass this, so

what we are being scared into is not fiber, it is not municipal deployment

of fiber, it is codifying the monopolies of the regional telephone company.

The regional telephone companies have spent hundreds of millions of dollars

fighting against municipal fiber deployment and municipal networks. They

have been successful in most cases, so we are being scared, but we are

being scared into a rabbit hole, not out into the great outdoors. It

is not a particularly pleasant view, but that is what is happening now.

I don't think that scaring is the right thing. And of course talking

about Congress and talking about logic is an interesting paradigm.

Isenberg: Paradox!

Bradner: There

are a fixed number of clues in the world and the population going up,

the density goes down. No clue ever visits Washington or any other capital.

This is a perfect example of it. What we are seeing now going on there

is this, Bush what did you do to make the kids bandwidth? And the answer

is, we asked the telephone companies to help.

Man: Nicely!

Bradner: No,

we begged the telephone companies

Isenberg: Right

up the road there is a boat yard called, Quissett Boat Yard, and they

have T-shirts that say, "We are all here because we are not all there."

I think that applies to Congress. I would like to give Roxane the last

word once again because she has been so insightful in the past but first

Frank caught 2 stripers and a bluefish tonight, a big blue fish 10 pounds.

Did anybody else catch any?

Man: Seaweed

-- a couple of stripers and some seaweed.

Isenberg: Somebody

caught salad. A striper. I think that everybody threw them back, right?

Did anybody catch any over 28 inches? No. Oh, the bluefish, yeah but

you threw it back. Fresh bluefish is good! Anyway, so there are more

fish to be caught at first light tomorrow morning. Anyway, Roxane, then

music, and then we will see you in the morning. Roxane, hit it!

Googin: Well

I hope everyone sleeps on this. I hope it doesn't take 3 to 5 year to

fix, cause we are all going to be living on our cash balances in the meantime.

I, for one, am convinced

that our capital markets aren't going to recover until we figure out what

to do. And optimistically enough, I think as soon as we do figure out

what to do, they will jump up a lot, because they are a discounting mechanism.

But their immunity to these tax cuts tells me, on the down side, that

this is something that everyone might benefit from putting their heads

together to figure out.

I do think that our

esteemed government is going to have a very hard time, and I think that

they will get involved, and I am afraid that they might side with the

wrong people. It is up to all of us to try to think about how we can

pull together to make some sub-optimal solution come out of this, since

there is no optimal solution.

I would just make

the observation that this move toward unlimited supply is moving beyond

bandwidth. Think about the symbiotic relationship between open source

software and the Internet, and how they work together, and how the Internet

helps foster the open source movement, and what economics this [synergy]

starts to impact. The software business is a very large business, and

it could be very negatively impacted by open source software. I'm not

passing a judgment on open source software. I happen to like some of

it. But it is a fact that it will be impacting our markets. Not as big

as the telecom issue because the business is smaller, it is not leveraged,

but it will redefine economics well beyond the bandwidth sector. So maybe

we can all sleep on it and pick this up tomorrow.

Man: And feel

better in the morning.

Isenberg: Well

thank you very much.

(return

to top)

page last modified: June 1, 2002

|